It was only a few months ago that 30 year fixed mortgage rates hit their record lows sinking beiow the 3.5% mark. Never in history had rates ever been that low! But with the stock market improving and investors jumping out of the bond market and into stocks, interest rates are staring to rise again.

From an historical point of view, it seems unreasonable to make an issue about 4% mortgage rates being something to be concerned about. Who hasn't heard the story often told by veteran homeowners about having an interest rate in the 10% to 20% range back in the 1980s? Compared to double digit rates, 4% is still something that people should be absolutely thrilled about.

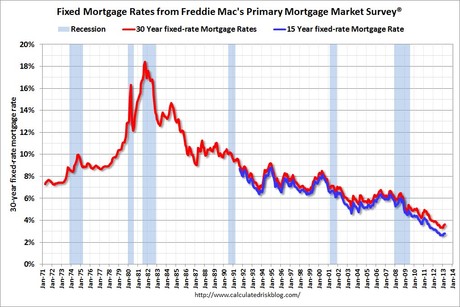

Take a look at the history of mortgage rates over the past 40 years.

The Big Bear real estate market is no different from anywhere else when it comes to affordability. One can only buy a house they can afford, especially with today's strict lending standards. The two factors that determine the affordability of home ownership are the home's price and the mortagage's interest rate. (Keep in mind that about 30% of Big Bear sales are cash; the rest require financing.) So regardless of how low the current rates are, let's consider the impact that an increase in mortgage rates might have on home prices.

Let's base our example on a purchase price of $200,000, as that is a convenient number inbetween the current median sale price of $187,000 and average sale price of about $250,000 here in Big Bear.

A $200,000 home at 3.5% interest results in a mortgage payment of about $900. If the rate goes up to 4%, the home price would have to be $188,000 to result in that same $900 payment. If the rate goes up a full point to 4.5%, that home price would have to drop to $178,000 to end up with a $900 payment.

In short, an increase in the mortgage rate of .5% means that the home price will have to drop 6% to stay at the same payment and an increase of 1% in the interest rate means the home would have to drop 11% to result in the same $900 payment.

So to the effect that interest rates rise, home prices will receive downward pressure.

This does not mean that the price of homes in Big Bear will drop. But it does suggest that any gains that the real estate market would have realized at the lower 3.5% interest rates will likely be marginalized to a certain extent at the higher rate. To what extent depends on many other economic factors.

On a national scale, the Federal Reserve understands that these increasing interest rates might hamper growth in real estate and are poised to take action to stabilize rates if need be. Many financial experts have suggested that the Federal Reserve will likely take action to keep rates somewhere between 4% and 4.5% for the foreseeable future to make sure that the recovery in the real estate market stays robust.

Ultimately, in reviewing the interest rate chart above, even with mortgage rates creeping higher, you can hardly find a better time in history to purchase a Big Bear home than now!